Wednesday’s Consumer Price Index (CPI) inflation report for July came in as expected — and it gives a clear pathway for the Federal Reserve to cut benchmark rates for the first time since starting its aggressive rate-hike cycle in early 2022.

The history of global pandemics shows inflation rising at first, as supply chains don’t operate well in this environment, but disinflation happens after that. The disinflation that typically comes after a pandemic fades away without deflation occurring.

With the national unemployment rate rising, job openings declining, jobless claims rising and wage growth slowing, the first Fed rate cut of this cycle is set for next month. Even with that first cut, the Fed is still pushing restrictive policy and is far from having a neutral policy. So, let’s look at today’s inflation report and see why this sealed the deal for a September rate cut.

From the U.S. Bureau of Labor Statistics (BLS): The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.2 percent on a seasonally adjusted basis, after declining 0.1 percent in June. … Over the last 12 months, the all items index increased 2.9 percent before seasonal adjustment.

The next sentence of this report is even more interesting:

The index for shelter rose 0.4 percent in July, accounting for nearly 90 percent of the monthly increase in the all items index.

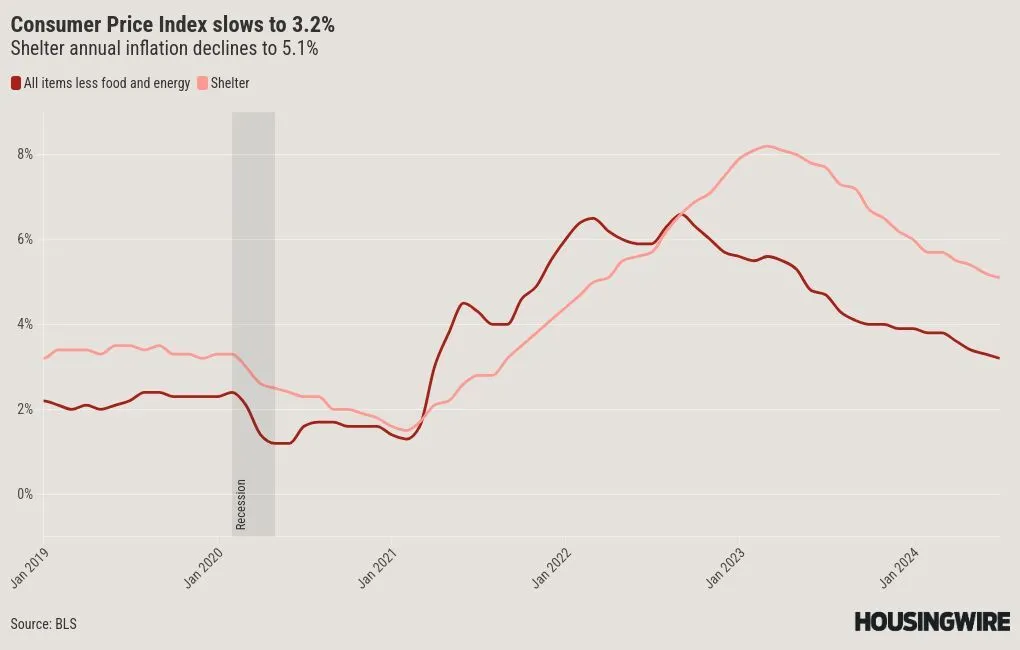

Housing inflation is slowly decreasing — as the chart below shows — but we all know this dataset lags a bit. The Fed also understands this, which is why it has talked a lot about CPI inflation lately, knowing that there are more disinflation variables in the CPI versus the Personal Consumption Expenditures (PCE) inflation data. HousingWire Editor in Chief Sarah Wheeler and I talked about this recently as we were getting ready for inflation week.

Labor over inflation

Remember that the Fed cares more about core inflation — and housing accounts for 45.1% of CPI inflation, so it matters a lot. Shelter inflation is cooling down, and it had to for core inflation to fade. With wage growth slowing and more housing supply coming online, it’s hard for the inflation metric to accelerate like it did during the COVID-19 pandemic.

Headline CPI inflation was running above 9% in June 2022. The same data in today’s report is running at 2.9% on a year-over-year basis, so progress has been made. But while inflation isn’t the primary driver of the recent talks about rate cuts, it has given a clear pathway for a pullback because labor data is getting softer.

Clearly, we have made good progress on inflation for some time without rate cuts, but we will finally get our first cut in September. This is happening because the labor market is getting softer based on the data lines the Fed tracks.

It’s not only because the unemployment rate increased to 4.3% in July, up from 3.5% one year earlier. Job openings are down and the quit rate is at pre-COVID levels. Meanwhile, wage growth has slowed and is getting closer to the Fed’s target of 3% per year.

The recent move to lower mortgage rates is happening as the labor data cools. If the Fed starts the rate-cut cycle and the labor data gets softer, mortgage spreads can further improve in 2024 and 2025. This means sub-6 % mortgage rates and the possibility of rates below 5%.

The first rate cut is coming as mortgage rates have already moved 1 percentage point lower than their recent peaks. Looking ahead to the rest of 2024 and into 2025, the labor data will increasingly run the show if it continues to weaken.

Now that headline CPI inflation is below 3% — and below the running average of 3.3% since 1914 — it’s time for the Fed to ensure that the labor data doesn’t break and we have a job-loss recession.